What is Income Tax Return (ITR)? How to File ITR Online for FY 2024-25 (AY 2025-26)?

Filing income taxes is always regarded as a difficult task. However, it is not as tiresome as it appears. The Income Tax Department is working hard to make the filing procedure simple and straightforward.

The Income Tax Department has likewise embraced digital technology, and one of the key benefits is electronic filing (ITR e-filing).

From implementing the provision u/s 234F for non-filers of income tax returns to making the majority of the processes available online, the department’s goal is clear: it wants your files to be clean and consistent with the law.

While filing an ITR, several questions arise, such as how to file an ITR. Which is the correct ITR form to select? What documents are necessary to file the ITR? Can I file an ITR for fiscal year 2024-25 (AY 2025-26)? There are numerous.

This article will provide you with the latest information and updates you need to know when completing your income tax return (ITR) for Fiscal Year 2024-25 (AY 2025-26).

Budget Update, 2025

There’s no income duty on periodic income up to ₹ 12.75 lakh!

The government increased the Section 87A refund outside from ₹ 7 lakh to ₹ 12 lakh, offering significant duty relief for the middle class. Salaried individualities can claim a standard deduction of ₹ 75,000, making inflows up to ₹ 12.75 lakh duty-free.

New Slab Structure Under the New Tax Regime

- ₹ 0- ₹ 4 lakh No duty

- 5 for ₹ 4 lakh to ₹ 8 lakh,

- 10 for ₹ 8 lakh to ₹ 12 lakh,

- 15 for ₹ 12 lakh to ₹ 16 lakh,

- 20 for ₹ 16 lakh to ₹ 20 lakh,

- 25 for ₹ 20 lakh to ₹ 24 lakh, and

- 25 for ₹ 24 lakh and beyond. 30

- Extended time to file streamlined returns( ITR- U)

Taxpayers now have four times( rather of two) to revise their income duty returns.

You can calculate your estimated income duty after the emendations made in Union Budget 2025 then.

What is the Income Tax Return (ITR)?

Governments levy income taxes on individuals, corporations, and other entities. The tax is often computed as a percentage of income received, and the proceeds are used to pay various government programs and services.

eFiling of Income Tax Returns refers to the electronic submission of tax returns via online platforms supplied by tax authorities. It provides an alternative to the usual technique of filing paper-based tax returns. You can easily and quickly file an income tax return from the convenience of your own home or office.

Individuals must pay income tax on their salary or earnings, as well as on other types of income such as interest, dividends, rental income, corporate profits, and capital gains. Corporations also have to pay income tax on their profits.

ITRs contain all of the data of an individual’s income and tax-saving investments for a certain fiscal year. The tax department has issued seven types of ITR forms for filing income tax returns, namely ITR 1, ITR 2, ITR 3, ITR 4, ITR 5, ITR 6, and ITR 7.

What Are the Advantages of Filing an Income Tax Return?

In India, it is customary for citizens to submit an Income Tax Return (ITR) if their gross income surpasses the basic tax exemption amount of 2,50,000, subject to specific requirements. You are not required by law to file your return if your annual income is less than Rs 2,50,000. However, due to the advantages of submitting an income tax return, it is still advised that you do so:

Unintentional ClaimsWhen determining the value of an accident claim, income tax returns may be utilized as supporting documentation. The precise formula, however, as well as additional elements including the extent of the injury, associated medical costs, and loss of earning potential, will be taken into account. | Evidence of Income or Net WorthITR is a trustworthy source of proof of income since it provides a thorough account of a person’s earnings, deductions, and tax obligations. | reimbursementif you have paid too much or had too much TDS withheld, you are entitled to a reimbursement. Receiving your money back from the Income Tax Department is the greatest happiness in the world. |

Qualifications for a Loan ApplicationOne of the fundamental documents needed for loans is the last three years’ worth of income tax returns. This aids banks in determining your ability to repay. | Forward capital lossesYou have the option to carry forward and settle capital losses that you have accrued throughout a fiscal year. | Getting a VisaMany foreign consulates require you to provide your income tax returns from the previous three years or the current year in order to go overseas. Your chances of obtaining a visa may be lowered if you have no return, particularly if you fall under the visiting, investor, or work permit categories. |

Losses carried forwardDo you want to claim the company loss from last year? All you need to do is file your income tax return. | Regarding Startup CapitalAre you trying to raise money from angel or venture capitalists? Make sure you have current income tax returns. Your tax returns are used by many investors to evaluate the profitability, scalability, and other financial aspects of your company. | Defense Against Black MoneySince any income that is not disclosed to the Income Tax Department is considered black money, your savings will never be in danger of being labeled as such by the tax authorities if you diligently complete your income tax return each year. |

Purchasing insurance High-life insurance policyWhile offering expensive life insurance, some insurance firms insist on income tax records in order to confirm your yearly income. | Getting a Government ContractOccasionally, submitting your income tax return is required when applying for government contracts, particularly when high-value contracts are being awarded. | Stay out of troubleYou risk getting into problems with the Income Tax Department if you fail to file your income tax returns. You run the danger of having to pay interest on it in addition to the penalty. |

Application for a Credit CardDo you want to show off your high-limit credit card? Having a large credit limit on a credit card is made possible by income tax returns. | Development of the countryBy submitting an income tax return, you can contribute to the process of nation-building. |

What is the income tax return filing deadline?

For FY 2024–25 (AY 2025–26), the ITR filing deadline is July 31, 2025. In order to preserve correct financial records, avoid penalties, claim timely refunds, comply with tax rules, and facilitate financial transactions, it is imperative that ITRs be filed on the due date. Prioritizing timely filing is advised in order to comply with regulatory obligations and prevent needless problems.

However, the deadline is October 31 for those who are subject to a tax audit, and November 30 for those who are subject to transfer pricing following the fiscal year’s conclusion.

- individuals operating a business with sales or turnover of more than Rs. 10 Cr.

- a professional who generates gross receipts of more than Rs 50 lakhs.

- a person operating a business or profession in accordance with section 44AD whose sales or turnover above Rs 2 Cr. or who

- reports revenue that is less than the deemed income under the relevant section.

For whom is an income tax return appropriate?

When total income over the basic exemption threshold, all Indians, even non-resident individuals, must file an income tax return. The basic exemption limit for filing an Income Tax Return (ITR) under the Old Tax Regime (Opt-in) differs depending on the age group. The barrier is established at Rs. 2.5 lakh for anyone under 60. Super senior citizens, who are 80 years of age or more, have an exemption limit of Rs. 5 lakh, while senior seniors, who are 60 to 79 years of age, have an additional exemption limit of Rs. 3 lakh. Rs. 3 lakh for seniors and those under 60, while keeping the cap at Rs. 5 lakh for really senior folks.

Whether or whether you have paid taxes, you still need to file a return. You must therefore file an income tax return even if your employer has fully deducted TDS.

However, there are additional circumstances besides income exceeding the Basic Exemption Limit that would necessitate filing an ITR!

These circumstances are:

- If the company’s turnover surpasses Rs. 60 lakh

- If an individual practices a profession and their professional receipts surpass Rs. 10 lakh

- If the total amount of TDS and TCS surpasses Rs. 25,000

- If there are more than Rs. 50 lakh in total deposits in one or more savings accounts

- If the total amount deposited in one or more current accounts surpasses one crore rupees

- If the annual cost of foreign travel exceeds Rs. 2 lakh

- If a year’s total electricity costs surpass one lakh rupees

- if a person is the beneficiary of an asset situated in a foreign nation or receives income from foreign assets.

Which Documents Are Needed to Submit an ITR?

There are a few documents that are typical when completing an ITR, even if they vary depending on the source of income. Additionally, keep in mind that you are not needed to upload or submit any of the documents on the internet; it is recommended that you keep them on hand to ensure that the necessary information is filled out accurately, save time, and prevent common mistakes.

Simple Documents:

Permanent Account Number, or PAN Card.

Aadhaar Card: Required for electronic filing.

Bank Statements: Account statements or passbooks that show interest income.

Form 16: Employer-issued for salaried individuals.

Documents Associated with Income:

Forms 16A, 16B, and 16C: For revenue from fixed deposits, real estate transactions, and rent, use Forms 16A, 16B, and 16C, respectively.

Form 26AS: Tax credit statement displaying TDS/TCS and advance tax paid is Form 26AS.

Salary slips: To view information about earnings and deductions.

Proof of Income: revenue from a business, rental income, or other sources.

Documentation of Investments:

That Save Taxes: Under Sections 80C, 80D, etc.

home loans Statements : for principal and interest payments on home loans.

Capital Gains Documents: For the selling of shares or other assets.

Investment proofs: include stocks, mutual funds, and other assets for tax purposes.

Additional Documents:

Interest certificates: can be obtained from post offices or banks.

Receipts for loan repayment: For educational or other debts that qualify for a deduction.

Receipts : for life and health insurance premiums.

Particular Situations:

Foreign Income Documents: For individuals who earn money overseas or who are NRIs.

Rent Agreements: To assert exemptions under the HRA.

Receipts for charitable donations: For Section 80G deductions.

Verify the entire list of documents required for filing an ITR if you get income from capital gains, real estate, salaries, and other sources. A more seamless ITR filing process is ensured by having these documents on hand. Use Tax2win to file your ITR.

How do ITRs for FY 2024–2025 (AY 2025–2026) get filed?

The ability to electronically file an income tax return is made available by the income tax department. However, a few things must be taken into account before to filing the ITR: –

- Collect the required paperwork: Gather all the necessary paperwork for your ITR, including bank statements, investment proofs, Form 16 (TDS certificate), and any other supporting documentation for your income, deductions, and exemptions.

- Select the relevant ITR form: Based on your residential status, sources of income, and other variables, choose the appropriate ITR form. Various ITR forms (ITR-1 to ITR-7) are available in India for various taxpayer categories. Make sure you use the appropriate form for your particular circumstance.

- Determine your taxable income: Determine your total income for the fiscal year by taking into account all of your revenue sources, such as capital gains, rental income, business income, salary, and other income. To determine your taxable income, subtract the appropriate exemptions and deductions.

- Complete the ITR form: Complete the chosen ITR form completely, including all necessary information about your personal background, income, deductions, taxes paid, and other pertinent factors. To prevent any inconsistencies, be sure to enter the correct information.

Step 1: Enter your user ID and password to access the e-filing portal.

Step 2: Select e-File > Income Tax Returns > File Income Tax Return from your Dashboard.

Step 3: Click Continue after choosing Assessment Year 2025–2026 and Online Filling Mode.

Step 4: Click Resume Filing if your income tax return has already been completed and is awaiting submission. Click Start New Filing if you want to start the return preparation process over and remove the saved return.

Step 5: To continue, choose Status if it applies to you and click Continue.

Step 6: When choosing the form of income tax return, you have two options:

- Choose the ITR form if you know which one to file; if not,

- You can click Proceed after choosing Help me determine which ITR Form to file if you’re unsure which one to file.

- Here, you can proceed with filing your ITR after the system assists you in determining the correct ITR.

Take note:

- Your responses to a series of questions will help you determine which ITR or schedules apply to you, as well as your income and deduction details, and will assist you in filing your ITR accurately and without errors.

- You can skip these questions if you already know the ITR, the schedules that apply to you, or the specifics of your income and deductions.

Step 7: After choosing the ITR that applies to you, take note of the required document list and click Let’s Get Started.

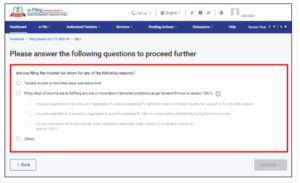

Step 8: Click Continue after checking the box that corresponds to your justification for submitting an ITR.

Step 9: In the Personal Information Section, choose Yes if you want to choose the New Tax Regime. Please take note of the pop-up notification stating that the new tax regime does not allow for certain deductions and exemptions. Examine your previously entered data and make any necessary edits. If necessary, enter the remaining or extra data. At the conclusion of each section, click Confirm.

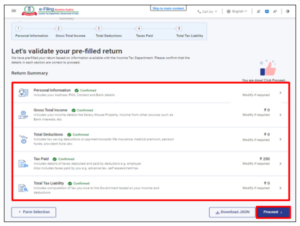

Step 10: Fill out the various areas with your income and total deductions. Click Proceed once you have filled out and verified every section of the form.

Step 10a: If a tax liability exists

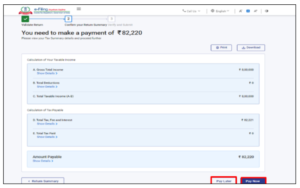

You will see a summary of your tax computation based on the information you have provided after selecting Total Tax Liability. The Pay Now and Pay Later choices will appear at the bottom of the page if the computation indicates that there is a tax liability.

Take note:

Using the Pay Now option is advised.

You can pay after filing your income tax return if you choose to pay later, but you run the risk of being deemed in default and may be required to pay interest on the tax that is owed.

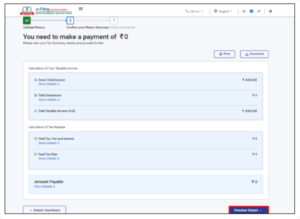

Step 10b: If you are qualified for a refund or if there is no tax liability (no demand or refund),

Select Preview Return. You will be directed to the Preview and Submit Your Return page if there is no tax due to pay or if you receive a refund based on tax computation.

Step 11: You will be taken to the e-pay Tax service if you select “Pay Now.” Click “Continue.”

Take note:

Clicking Continue will lead you to the portal’s e-Pay Tax page where you can pay taxes. To find out more, consult the e-Pay Tax user instructions.

Step 12: A success notification appears following a successful payment made using the e-filing portal. To finish filing your ITR, click Back to Return Filing.

Step 13: Click Preview Return.

Step 14: Click Proceed to Preview after checking the declaration checkbox on the Preview and Submit Your Return page.

Note: You can leave the TRP text boxes empty if you did not use a tax return preparer or TRP to prepare your return.

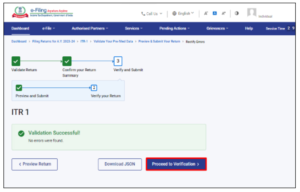

Step 15: Click Proceed to Validation after previewing your return.

Step 16: Click Proceed to Verification on the Preview and Submit your Return page after it has been verified.

Note: You must return to the form to fix any issues if a list of them appears in your return. By selecting Proceed to Verification, you can e-Verify your return if there are no mistakes.

Step 17: Click Continue after choosing your preferred option on the Complete your Verification page.

Verifying your return is required, and the simplest method to do so is by e-Verification (the suggested choice, e-Verify Now). This method is faster, paperless, and safer than mailing a signed physical ITR-V to CPC via speed post.

Note: You can file your return if you choose to e-Verify Later, but you will need to confirm it within 30 days after submitting your ITR.

Step 18: Click Continue after choosing the method to e-Verify the return on the e-Verify page.

The Transaction ID and Acknowledgment Number are shown along with a success message once you e-verify your return. Additionally, a confirmation message will be sent to the email address and mobile number you registered with on the e-filing platform.

How Can I Use Tax2win to File an ITR?

With Tax2win, filing your income tax return is simple and straightforward. Tax2win provides extensive tax-related services and streamlines the Income Tax Return (ITR) filing procedure. It makes it simple for anyone to file their ITR online with an intuitive UI and detailed instructions.

| Step 1: go to the tax2win website. Click the “File ITR Now” option here. | Step 2: Choose your revenue source and press “Continue.” | Step 3: Simply upload your Form 16 if you are a salaried individual. You can bypass this option and continue if you don’t have a form 16. | Step 4: Enter the Aadhaar and PAN information, the financial year, and other fundamental information such as your bank account information, employment information, income information, and any deductions. After providing all the information, enter your pre-paid taxes. | Step 5: Click “File My ITR” after reviewing your tax computation. And it’s finished! |

What Happens After Income Tax Returns Are Electronically Filed?

After completing the electronic filing of your income tax return, you need to:

- You will receive a notification that your income tax return was successfully filed, along with an email attachment called ITR-V (Acknowledgment). Check your inbox for the email address you supplied on your income tax return form.

- Verify all of the figures in your completed ITR form or ITR-V to be sure there are no errors or mistakes.

- You can e-Verify online or send a hard copy of the income tax return to CPC Bangalore to confirm it. The return filing process concludes here after the return has been satisfactorily verified. Your work is now finished.

- If your tax return includes a refund, you should expect to receive it in your bank account in the coming days. To avoid missing any crucial departmental updates, it is best to continue monitoring the status of your income tax return.

- Here, you can see the status of your refund.

How can I use Form 16 to e-file my ITR?

In just three easy actions, file your income tax return with us:

Upload Form 16: Choose your income sources on our e-filing platform, then upload Form 16.

Review: Our sophisticated program gathers the necessary data and completes your information on its own. Just go over the details.

File ITR: Your income tax return is filed online by our system as soon as you confirm.

More information on Form 16 can be found here.

If I have taxable income but fail to file my income tax return, what would happen?

You may face penalties from the Income Tax Authorities if you have taxable income and fail to file an income tax return. Be ready to accept fines and penalties as well as letters from the Income Tax Department. The repercussions of failing to file a return are:

a fee under section 234F: Late submission If the return is not filed on or before the due date, a fee under section 234F will be assessed. The amount of costs will change based on when you file your return and how much you make. The highest amount that can be charged is Rs. 5000.

Notice u/s 142(1): If you haven’t filed your return by the deadline, you must do so in accordance with Notice u/s 142(1).

If you disregard this notice, you could face

- (a) a Best Judgment Assessment under section 144,

- (b) a fine of Rs. 10,000 under section 271(1)(b), or

- (c) imprisonment under section 276D with or without a fine.

Notice under Section 148 for providing a return within the time frame specified in the notice.

According to Section 270A, if income is underreported because of:

- Inaccurate disclosure or misreporting, the penalty will be 200 percent of the tax due on that income; Otherwise, the penalty will be 50 percent of the tax due on that income.

- Penalties for income concealment under s. 271(1)(c) range from a minimum of 100% to a maximum of 300% of the tax amount.

- Until you file your return, interest under section 234A continues to accrue at the rate of 1% every month or a portion of the month.

- Additionally, if you failed to comply with the advance tax rules at the time of the late filing of your return, you would be forced to pay interest under sections 234B and 234C, both of which are assessed at a rate of 1% each month or a portion of the month.

- Should you wish to carry over business or capital losses, you will not be able to do so if you fail to file an income tax return or if you file after the deadline.

Now that you know how to submit an ITR online, you should also know that there are a number of ways to reduce your tax liability. However, careful preparation is necessary to maximize these exemptions and deductions. Tax planning might be a little challenging because there are so many ways to reduce taxes. Do not be concerned! Our professionals will assist you save as much money as they can. To begin tax planning, just schedule a Tax2win tax professional.

Commonly Asked Questions

Q: Can I file now since I didn’t file my ITR for AY 2022–2023?

Yes, even if you didn’t file it at first, you can still file an Updated Return (ITR-U) for the Assessment Year (AY) 2022–2023. Within 24 months following the conclusion of the applicable assessment year, taxpayers are permitted by the Income Tax Department to file ITR-U. As a result, you have until March 31, 2027, to file your ITR-U for AY 2022–2023.

Q:What would happen if I filed my income tax return incorrectly or beyond the deadline?

missed the deadline:

A belated return may be filed three months before the end of the applicable assessment year; for example, for 2024–2025 (AY 2025–256), the filing date would be December 31, 2025. It is referred to as a belated return, which is a return that was filed after the deadline but with late costs paid in accordance with Section 234F.

Erred:

Three months before the relevant assessment year, that is, on December 31, 2025, for the 2024–25 (AY 2025–26) filing, you can amend your previously filed ITR.

Q: What options are available to an individual who wishes to file a tax return after the income tax return filing deadline has passed or who misses the due date?

One can still file a late or belated return even if they miss the deadline. Three months before the applicable assessment year, a delayed income tax return may be submitted. You have until December 31, 2025, to file the 2024–2025 ITR (AY 2025–26) as a delayed return.

Q:Can I electronically file my ITR without Form 16?

You can use other papers, such as pay stubs, bank accounts, investment statements, and other records to determine your total income and taxes paid, if you do not have Form 16. Additionally, Form 26AS, which may be accessed from TRACES via the Income Tax Portal, provides details regarding your TDS and TCS.

Even without Form 16, you can electronically file your income tax return. After completing the necessary information in the software, you must submit the ITR.

Q: How long does it take to complete the e-Verification of an Income Tax Return?

You have 30 days from the date of filing your income tax return to complete the verification process by signing it manually or electronically. You can find out the specifics of both methods here. There are several ways to e-verify ITR: via Net banking, bank ATM, digital signature certificate, Adhaar OTP, bank account number, demat account, and physically sending ITR-V. Read the full e-verification guide.

Q:What is the most recent change made to Section 234F, namely the penalties for filing an income tax return after the deadline and the other repercussions for failing to file or filing an income tax return after the deadline?

It is crucial that returns are submitted by the deadline in order to enhance tax compliance and the efficient use of data in tax administration. In light of this, the law levies the following penalties under s. 234F in the event that returns are not filed on time:

If a return is filed on or before the due date, which is July 31*, there are no fees; if a return is filed after the due date but before December 31*, there are fees of up to Rs. 5,000 * (if an extension is granted, these dates will be replaced by the extended date).

NOTE: If your total income is up to Rs. 5 Lacs, you will always be penalized Rs. 1,000, regardless of when you file your return. Additionally, provisions pertaining to fees for late filing of income tax returns are only applicable starting with the Financial year 2018-19 (Assessment year 2019–20).