As the name implies, section 139(8A) permits persons to file a missing return or correct any filing errors by filing an updated return (ITR-U). The Union Budget 2022 introduced the idea of ITR U, or the updated return.

Updated Budget for 2025

- The two-year period for filing an Updated Income Tax Return (ITR-U) has been extended to four years as of April 2025. Like a Revised ITR, an Updated ITR cannot be used to claim deductions or lower tax liability; it can only be submitted to disclose more income and increase tax liabilities.

- For instance, a taxpayer might have filed an Updated ITR at any time between January 1, 2025, and March 2027 if they had already filed an ITR for FY 2023-24 (Assessment Year 2024-25). The deadline has been extended to March 31, 2029, due to this budget modification.

What is an Updated Return, or ITR-U?

- For people who have not submitted their ITR or who have overlooked or misreported income on prior returns, the ITR U, or Updated Income Tax Return form, is a lifesaver. According to Budget 2025, taxpayers have up to four years from the end of the relevant assessment year to update their return using the ITR-U form, which enables them to fix mistakes or omissions on their ITRs. The conclusion of the pertinent assessment year is used to compute these four years.

- For example, if you failed to file your ITR for FY 2021–2022 (AY 2022–2023), you have until March 31, 2027, to file an amended return. There may be legal repercussions if this final opportunity is missed. Save the ITR-U file.

- The taxpayer has up to two years of the relevant assessment year to file an ITR-U, regardless of whether they filed an original, amended, or belated ITR or if they failed to file the ITR at all in a certain fiscal year. Note that the ITR-U filing period for AY 2024–2025 began on January 1, 2025.

Please take note: It is also suggested that if a notice to show reason under Section 148A of the Income Tax Act is sent out more than 36 months after the conclusion of the relevant assessment year, no amended return will be permitted. Nonetheless, an amended return may still be submitted within 48 months of the conclusion of the applicable assessment year if an order is issued under Section 148A(3) stating that it is inappropriate to issue a notice under Section 148. This clause guarantees taxpayers flexibility and transparency, especially in cases when section 148 determines that more investigation is not necessary.

Who Can train Form ITR- U?

Any taxpayer is eligible to file an streamlined return under Section 139( 8A), anyhow of whether they’ve submitted an original, revised, or delinquent return. This allows individualities to correct any deletions, crimes, or inaccuracies in their preliminarily filed income duty return.

You can file an streamlined Return if :

- No return was filed preliminary

- Income wasn’t reported rightly

- Incorrect heads of income were named

- Carried forward losses need to be reduced

- Unabsorbed deprecation needs to be acclimated

- duty credit under Section 115JB/ 115JC needs to be reduced

- An incorrect duty rate was applied

Who Can not Submit an ITR U u/ s 139( 8A) Form?

In agreement with section 139( 8A), an streamlined Return can not be submitted if:

- If a revised return has formerly been submitted

- If the return of loss is an streamlined return

- If the income duty liability in the preliminarily filed return is reduced by an streamlined return

- If the revised return raises the quantum of the refund

- If Section 132 has been used to start a hunt

- if the Income Tax Department requests books of accounts or any other papers in agreement with section 132A.

- If the check was carried out in agreement with section 133A

- still, reassessment,re-computation, If there are any ongoing or finished assessment.

- The assessees has been informed if the Assessing Officer has information against the existent in agreement with the Prevention of plutocrat Laundering Act, Black Money( Undisclosed Foreign Income and means), duty of Tax Act, Benami Property Deals Act, or Bootleggers and Foreign Exchange Manipulators Act.

- still, and the information was attained by an arrangement mentioned in section 90 or section 90A, if the information for the applicable assessment time was handed to the existent before the date of return furnishing under this paragraph.

fresh Notified individualities

ITR-U Deadline for Filing: Time Restriction and Due Dates

As stated in budget 2025-26, the deadline for filing an amended return under section 139 (8A) has been extended from two years to four years beginning in April 2025 from the conclusion of the applicable assessment year. Therefore, until March 31, 2029, the amended return for FY 23-24 (AY 2024-25) may be submitted.

For Example,

Year of Assessment | Date of Updated ITR Submission Deadline |

| FY 2021-22 (AY 2022-23) | 31 March 2027 |

| FY 2022-23 (AY 2023-24) | 31 March 2028 |

| FY 2023-24 (AY 2024-25) | 31 March 2029 |

Download the ITR-U Form

ITR-U Penalty for Late Filing: How Much Will You Pay in Additional Tax?

The two-year period for filing an Updated Income Tax Return (ITR-U) has been extended to four years as of April 2025. Penalties for filing the ITR-U after the deadline are as follows: 25% more tax and interest is imposed if the return is filed within 12 months, 50% within 24 months, 60% within 36 months, and 70% within 48 months. Early filing will help prevent these additional expenses, but the revised timeline provides taxpayers more time to remain in compliance.

For Example,

| ITR-U was submitted within | Extra Tax |

| 12 months from the conclusion of the applicable AY | 25% extra tax (tax plus interest) |

| 24 months from the conclusion of the applicable AY | 50% extra tax (tax plus interest) |

| 36 months from the conclusion of the applicable AY | 60% extra tax (tax plus interest) |

| 48 months from the conclusion of the applicable AY | 70% extra tax (tax plus interest) |

How Can Form ITR-U Be Filed?

According to income tax regulations, an updated copy of the relevant ITR form (ITR 1–7) must be sent with the revised return (ITR-U).

ITR-U asks taxpayers for the following extra information:

- PAN, Aadhaar Number, Year of Assessment

- Has a return been filed for this assessment year before? (Yes/No)

- If so, If filed under 139(1) Others

- If applicable, provide the date of filing the original return (DD/MM/YYYY), the form filed, and the acknowledgement or receipt number.

- Do you have the right to submit an amended return? In other words, a person is not in a situation where filing an amended return is not possible.

- Choosing the ITR form to submit a revised return justifications for updating revenue.

- This covers factors like incorrectly reported income, previously unfiled returns, incorrectly selected heads of income, etc.

Are you filing an amended return 12 months after the relevant AY ended, or between 12 and 24 months after the relevant AY ended? - Are you submitting a revised return in order to lower your tax credit, unabsorbed deduction, or carried forward loss?

Part B: Updated income and tax payable (ITR-U) computation

- 1 (A) The income head under which the updated return states that additional revenue is being returned

- 1 (B) Total income according to the most recent valid return (only where the income tax return has already been filed)

- Total earnings according to Part B-TI

- The amount owed, if any (should be deducted from the amended ITR’s Part B-TT amount owed)

- Refundable amount, if any (to be deducted from Part B-TTI’s refund in the amended ITR)

- Based on the most recent legitimate return, the amount owed (only in applicable instances)

- 6. (i) Refund requested based on the most recent legitimate return, if any

- 6. (ii) Total Refund (including interest under 244A) as per the most recent valid return,

- if any obtained

Fee for failure to file income return under Section 234F of the Regular Assessment Tax, - if applicable

Total obligation for extra revenue

[25% or 50% of (9-7)] Additional income-tax liability on updated income - Net payable amount (9+10)

- Tax paid under section 140B

- Tax due dates are 11–12.

- Information about tax payments made on the amended return under Section 140B

- Information on Advance Tax, Self-Assessment Tax, and Regular Assessment Tax payments for which a credit has not been sought in the previous return (section 140B(2) prohibits granting credit for the same).

This includes relief under section 89, which was not sought in the previous return.

Do you wish to submit an ITR for a prior fiscal year? To guarantee a seamless ITR-U filing process, use an online CA.

How Can I Use Tax2win to File My ITR U?

Two kinds of ITR filings are available through Tax2win:

Do-it-yourself (self-filing)

DIY (Self-filing): If you know a little bit about taxes, you can file the ITR in four minutes by inputting some simple information. Because the Tax2win DIY platform is AI-integrated, it will automatically choose the appropriate ITR form for you, making filing incredibly simple.

Here are some easy steps to follow if you’re unsure how to file an ITR with Tax2win:

Step 1: Register for an account on the portal or use your current login information to access the tax2win website. Self-filing is only permitted for capital gains, company income, and salary income.

webpage for tax2win Step 2: A table listing every potential source of revenue appears after logging in. The sources of your revenue must be chosen. Tax2win’s DIY ITR filing system automatically chooses the appropriate ITR form based on your revenue sources.

Step 2: A table listing every potential source of revenue appears after logging in. The sources of your revenue must be chosen. Tax2win’s DIY ITR filing system automatically chooses the appropriate ITR form based on your revenue sources.

Step 3: Form 16 must be uploaded. You can just skip the option and continue if you don’t have Form 16.

Step 3: Form 16 must be uploaded. You can just skip the option and continue if you don’t have Form 16.

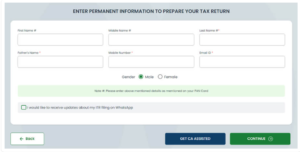

Step 4: Choose the year you wish to file the ITR for, then enter your DOB and PAN information. You will receive an OTP and a new account will be created if you do not already have a registered account with the Income Tax Department. Additionally, you can decide whether you want our do-it-yourself software to retrieve your personal information and pre-fill it.

Step 4: Choose the year you wish to file the ITR for, then enter your DOB and PAN information. You will receive an OTP and a new account will be created if you do not already have a registered account with the Income Tax Department. Additionally, you can decide whether you want our do-it-yourself software to retrieve your personal information and pre-fill it.

Step 5: In the following step, enter some basic information. A portion of it is pre-filled from the database of the Income Tax Department. Don’t forget to double-check the available data. You must input your personal information, including your name, email address, birthdate, father’s name, gender, and other facts, as seen in the image below.

Step 6: You must enter your employer category and address information in the following step. To further comprehend this, look at the graphic below.

Step 7: You must enter your employment information in the following step. For salaried employees, the standard deduction is applied automatically. You must enter your gross salary/CTC, standard deduction, professional tax under section 16, and exempted allowances such as HRA, LTA, gratuity, and net salary, as illustrated in the image below. Please take note that your employment information will be pre-filled in the ITR Form if you have uploaded Form 16. Verifying the information is all that is required before filing your ITR.

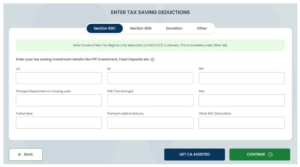

Step 8: To determine the relevant deductions, enter the specifics of the investment made during the year. Details of your PPF, LIC, PF, housing loan, FDR, NSC, tuition, annuity premiums, and other 80C deductions must be entered. Deductions such as 80D, 80CCD (1B), 80G, and others are also available.

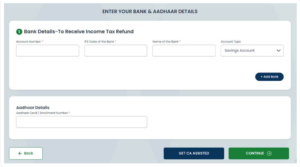

Step 9: Enter Your Bank Details

In this step, you need to provide your bank details, including your IFSC code, bank name, account number, and Aadhaar details. As per government regulations, submitting these details is mandatory. You also have the option to choose one account as your primary account, where your tax refund will be credited. Make sure to enter the correct details to avoid any issues with transactions.

Step 10: Upload your Form 26AS if you have it; if not, manually enter the information. Enter the information of your pay, taxes that have already been paid, such as self-assessment or advance taxes, taxes paid on your updated return, TDS paid on income other than salary, TDS on rental income, and TCS.

Step 10: Upload your Form 26AS if you have it; if not, manually enter the information. Enter the information of your pay, taxes that have already been paid, such as self-assessment or advance taxes, taxes paid on your updated return, TDS paid on income other than salary, TDS on rental income, and TCS.

Step 11: Choose ITR-U as the return filing type. Choose “not filed” if you haven’t submitted your ITR for this year. Choose “under section 139(1), fill in the details of the ITR filed, and click on continue” if you have already filed your ITR for this year.

Step 12: The software automatically calculates your tax burden under both the old and the new regimes based on the data you provided in the preceding sections. You can evaluate the two regimens and decide which is better for you.

Step 12: The software automatically calculates your tax burden under both the old and the new regimes based on the data you provided in the preceding sections. You can evaluate the two regimens and decide which is better for you.

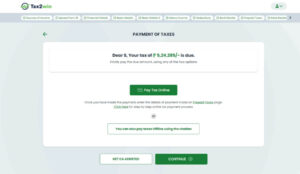

Step 13: You can now view the entire amount of taxes owed and choose to use the income tax portal to pay your taxes online. The income tax challan technique is another offline tax payment option. Press “Continue.”

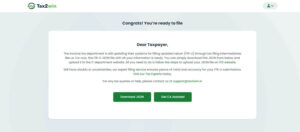

Step 14: You are now prepared to submit your ITR-U. If you are unsure, you can either obtain an eCA to file your ITR-U or download the JSON file and upload it to the Income Tax Department.

Step 14: You are now prepared to submit your ITR-U. If you are unsure, you can either obtain an eCA to file your ITR-U or download the JSON file and upload it to the Income Tax Department.

The following is the second method for filing an ITR on Tax2win:

Expert-Assisted ITR Filing.

Step 1 : Select “Hire eCA Now.”

Step 2: Choose the appropriate selections from the stages listed below.

Step 3: After choosing all pertinent income sources, click “hire now” to enlist the assistance of a qualified certified public accountant.

Step 3: After choosing all pertinent income sources, click “hire now” to enlist the assistance of a qualified certified public accountant.

How Can ITR-U Be Verified?

ITR-U can be confirmed using

Non-Tax Audit Cases:

- Aadhaar OTP

- For tax audit instances, an Electronic Verification Code (EVC) is provided.

- In non-tax audit situations, a Digital Signature Certificate (DSC) is used.

Tax Audit Cases :

- Digital Signature Certificate (DSC)

How Can I Determine How Much Tax Is Due on an Updated Return (ITR-U)?

The tax payable when submitting an amended return (ITR-U) consists of:

- Tax owed on extra income

- Interest charged for late payments

- Fee for late submission (if applicable)

- Extra tax to update the return

ITR-U Tax Calculation Formula:

- ITR-U is equal to Tax Due + Interest + Late Filing Fees + Extra Tax.

Net tax liability Formula:

- Total Income Tax Liability – (TDS + TCS + Advance Tax + Tax Relief) is the formula for net tax liability.

Fee for Late Filing (U/S 234F):

- If taxable income falls below ₹5 lakh, ₹1,000

- If taxable income exceeds ₹5 lakh, ₹5,000

- Not relevant when editing an ITR breakdown of total income tax liability that has already been filed:

Breakdown of Total Income Tax Liability:

Tax Due: Tax due on extra income recorded on Part B-TTI of the ITR-U

Interest : is assessed in accordance with Part B-TTI Sections 234A, 234B, or 234C.

Late Fee: Subject to Section 234F (where applicable)

Additional Tax: Depending on when it is filed, there may be a 25%–70% penalty.

Missed Returns ITR-U: What Takes Place If You Don’t File?

By submitting an updated return, CBDT gives you a third opportunity to comply with tax laws. If you fail to file the ITR, you will be deemed non-compliant and may be subject to penalties, interest, income tax notices, and other legal repercussions. If you fail to file your ITR and your income tax debt exceeds Rs. 25,000, you could face a minimum 6-month jail sentence, a maximum 7-year sentence, and a fine. If the tax liability is less than Rs. 25,000, you will be punished with a fine and harsh imprisonment for at least three months to two years.

Important Information Regarding ITR-U: Revised Return Purpose

ITR-U promotes compliance and helps taxpayers avoid penalties by allowing them to amend previously filed returns to reflect any missed income or deductions.

Window of Eligibility:

The deadline for filing an ITR-U is four years from the end of the relevant assessment year, as of April 2025.

One-Time Submission:

For a particular assessment year, an ITR-U may only be submitted once. Once filed under this clause, no more revisions are permitted.

Correction Types:

Errors in deductions, tax credits, or income adjustments are examples of corrections. However, reimbursement amounts cannot be increased or claimed via ITR-U.

Tax Payment:

To guarantee correctness and prevent inconsistencies, any extra tax and interest must be paid before filing the amended return.

No Refund Claims Allowed:

Refund claims cannot be made using ITR-U. Its main purpose is to correct filing errors and disclose additional income.

Learn the differences and specifics between ITR-U and Belated, Revised Income Tax Returns.

- Belated Return: You can file your ITR after the deadline and pay a penalty if you file your return after the deadline. Therefore, you can file a delayed return by December 31 of the specific assessment year if you missed the July 31 deadline.

- Revised Return: You have until December 31st of the specific assessment year to file a revised return if your initial or late return has mistakes, such as inaccurate income information or omitted deductions.

- ITR-U (Updated Return): Within four years following the conclusion of the applicable assessment year, taxpayers may amend or amend their previously filed ITRs. It cannot, however, be used to convey losses or request reimbursements.

The ITR

Deadline

Penalty

Belated ITR December 31st of the pertinent evaluation year - Rs. 1000 to Rs. 5 lakhs in income

- Rs. 5000 – Earnings over Rs. 5 lakhs

Revised ITR December 31st of the pertinent evaluation year No Penalty ITR – U (Updated) During the four years following the relevant A.Y. Additional ITR-U tax charges:

Within a year: 25% tax plus interest

Within 24 months: half of the interest and taxes

Within 36 months: 60% interest plus tax

Within 48 months: 70% interest plus tax

Having problems figuring out how much you owe on your updated ITR? Get complete ITR filing services, from computation to online ITR filing, by getting in touch with our tax professionals. Make a CA online reservation right now!

ITR-U FAQs

Q: What is Form ITR-U?

The Union Budget 2022 included a new form called the ITR-U, or Updated Income Tax Return. It enables taxpayers to fix mistakes or omissions made in earlier tax returns. Within two years of the conclusion of the applicable evaluation year, the form must be submitted. By giving taxpayers the chance to correct errors and guarantee conformity with tax regulations, this program seeks to improve accuracy and compliance in tax returns.

Q: Is it possible to file a nil return in ITR-U?

The following situations prohibit the filing of ITR U:

- If the total income is less than 2.50 lacs, the ITR U that needs to be submitted is a nil return.

- The tax liability will be smaller if ITR U is filed than if the original return was filed.

- If the ITR U that needs to be submitted is a loss return,

- The filing of ITR U will raise the amount of refunds.

- When the income tax authorities initiate actions under Section 132A,

- If the survey was carried out in accordance with 133A,

- In the event that a search or prosecution has begun,

- If there is an ongoing or finished assessment, reassessment, revision, or recalculation for that particular year,

Q: What is the income tax portal’s ITR utility?

A taxpayer can quickly file their ITR with the use of ITR utility software. Every year, a revised version of the ITR Utility software for online income tax return filing is released by the Income Tax Department.

Q: What advantages come with submitting Form ITR-U?

Even after the Original ITR, Belated ITR, and Revised ITR filing deadlines have gone or lapsed, taxpayers are still granted an extra four years to file their income tax returns.

Taxpayers can lower the likelihood of future tax notices and lawsuits by reporting and paying taxes on any missed income.

Compared to cases involving concealed income or income evading assessment, the tax liability and penalty under the updated return are lower.

Q: Does ITR U have any penalties?

When submitting an ITR-U, taxpayers are not liable to penalties or additional fees. They might, however, be subject to further taxation under Section 140B of the Income Tax Act. An extra 25% of the tax and interest is assessed if the return is filed within 12 months; 50% within 24 months; 60% within 36 months; and 70% within 48 months. Early filing will help prevent these additional expenses, but the revised timeline provides taxpayers more time to remain in compliance.

Q: Can we request a refund by filing ITR U?

No, you cannot file an ITR-U and receive an income tax refund. Under Section 139(8A) of the Income Tax Act, taxpayers can amend or rectify their tax returns in order to declare previously omitted income and pay the related tax by filing an ITR-U (Updated Return).

Q: When is the deadline for submitting an updated return for the academic year 2023–2024?

Four years after the conclusion of the applicable Assessment Year, an Updated Return must be filed. Therefore, March 31, 2028, four years after the end of March 31, 2024, is the deadline for filing an Updated Return for AY 2023–2024.

Q: When is the deadline for filing an AY 2022–2023 Updated Return?

Four years after the conclusion of the applicable Assessment Year, an Updated Return must be filed. Therefore, the deadline for filing an Updated Return in Form ITR-U for the academic year 2022–2023 is March 31, 2027, which is four years after the end of March 31, 2023.